Europe is entering a decisive phase for carbon capture and storage (CCS). Policy momentum is growing, industrial actors are announcing capture projects across multiple sectors, and cross-border transport and storage infrastructure is being planned.

However, as deployment accelerates, industry discussions keep circling back to two questions: Is the lack of CO₂ storage capacity the main bottleneck? How much of the challenge lies elsewhere in the value chain?

That question framed Carbon Management Europe's Projects Network side event held on 14 April 2026 ahead of the Knowledge Sharing Summit 2026, organised by Carbon Management Europe, Clean Air Task Force (CATF), and CaptureMap.

The session brought together storage developers, transport operators, and industrial emitters for what participants described as a “value chain reality check”.

A CCS pipeline with real momentum, and a geographic mismatch

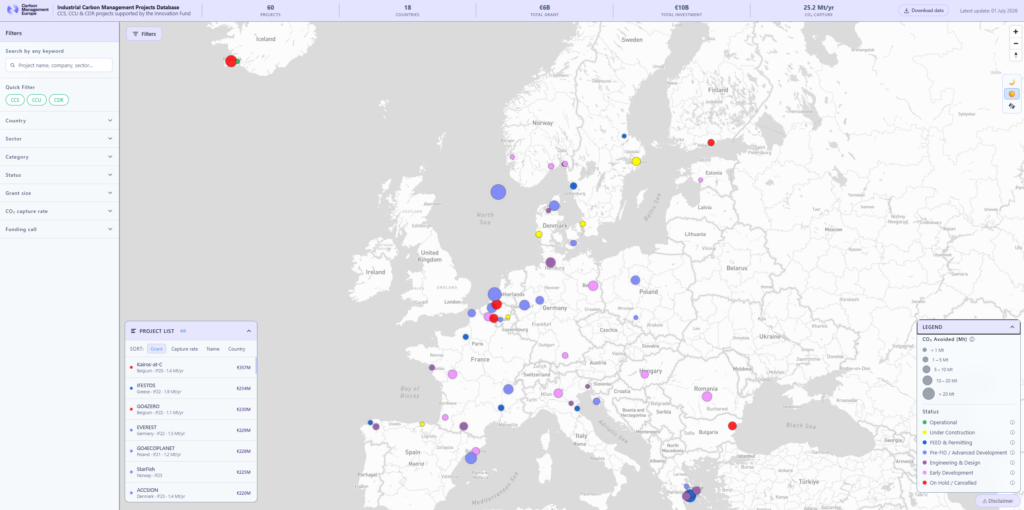

Carbon Management Europe’s EU Innovation Fund Industrial Carbon Management (ICM) projects database – sourced exclusively from the European Commission, CINEA, and official company sources – maps 60 Innovation Fund CCS and carbon capture and utilisation (CCU) projects across 16 European countries.

Figure 1 : Carbon Management Europe's EU Innovation Fund Industrial Carbon Management (ICM) projects database, mapping 60 ICM projects across 16 European countries.

Those projects could enable around 25 million tonnes per annum (Mtpa) of CO₂ capture capacity by 2035. Cement remains the largest sector represented, with 19 projects currently listed, highlighting the growing momentum behind industrial CCS deployment in Europe’s heavy industry sectors.

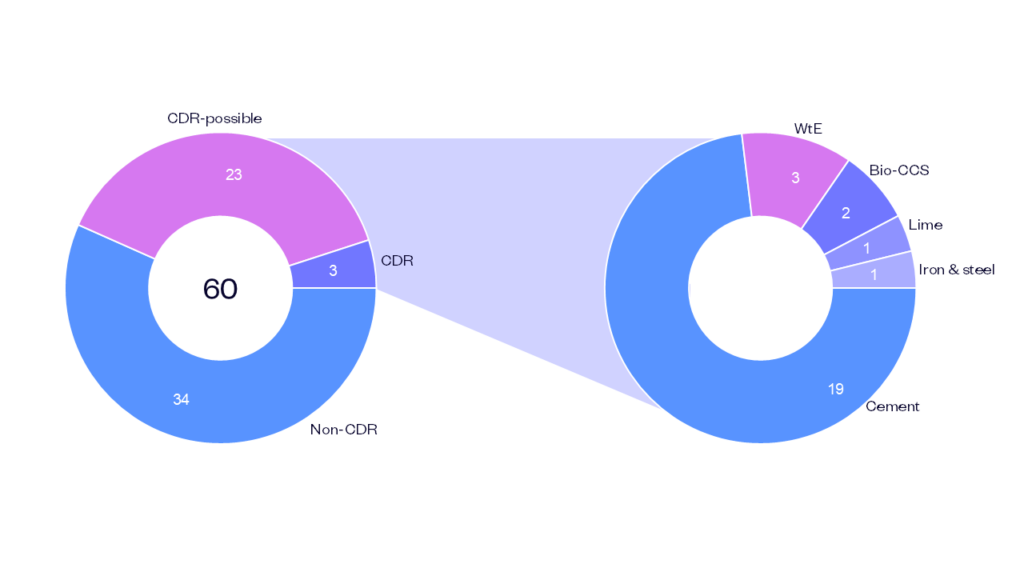

The scale of the carbon dioxide removal (CDR)1 opportunity through biogenic CO₂ capture from point source streams is significant. Among the Innovation Fund projects, 26 could contribute to CDR while decarbonising sectors including cement, lime, iron and steel, and waste-to-energy (WtE). Across Europe, 171 capture projects under development include biogenic CO₂ streams. According to CaptureMap data, if fully captured and permanently stored, these projects could deliver up to 47 Mtpa of carbon dioxide removals.

Figure 2: Breakdown of the 60 EU Innovation Fund Industrial Carbon Management projects by CDR potential and sector.

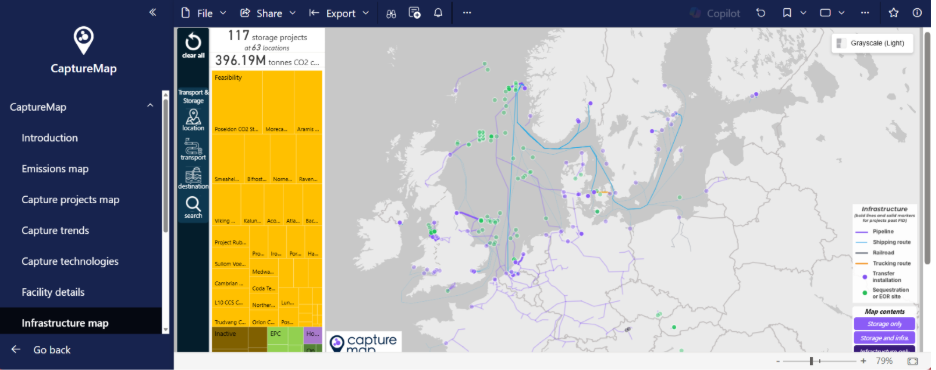

Capture Map’s data also reveals a structural mismatch that goes beyond a simple supply-demand imbalance. Planned storage capacity across Europe is more than double the combined capacity of current capture projects, suggesting that the headline storage numbers are not the core problem.

The challenge is both the geographical distribution and coordination across the value chain.

Capture projects are spread across the continent, while storage capacity is concentrated in a small number of countries. The UK, Norway, Denmark, and the Netherlands stand out as the principal cross-border storage providers, with Italy, Poland, and Iceland also showing surplus capacity.

Meanwhile, major industrial economies, including France, alongside Belgium, Sweden, and Finland, have no active storage projects and will depend on cross-border solutions to realise their capture potential.

This asymmetry creates a coordination risk. Storage developers are reluctant to commit infrastructure without confirmed capture volumes, while capture developers need confidence that storage access will be available before taking FID.

Figure 3: CaptureMap's European CCS infrastructure map

Eric Rambech, co-founder of CaptureMap, argued that as CCS deployment accelerates, companies need better data to act faster and with more confidence.

The challenge is not only whether enough storage capacity exists, but whether actors across the value chain have the market intelligence needed to understand where projects are emerging, how timelines align, and where coordination gaps remain. Better project-level data and market transparency will be essential to support cross-border collaboration and help companies move from opportunity mapping to action.

Unlocking CDR investment: From financing gap to market solution

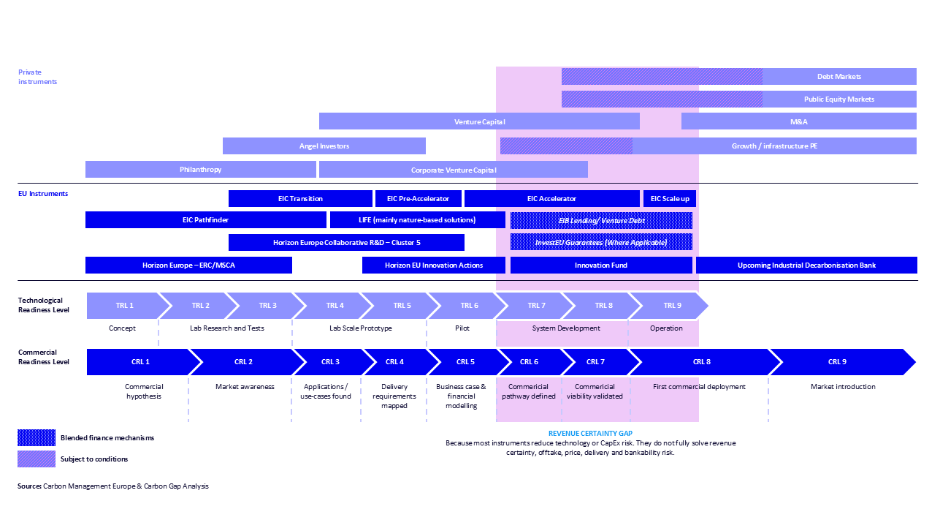

A highlight was discussions on how to mobilise private capital for CDR projects. Carbon Management Europe presented a practical roadmap for bridging the gap between early-stage public funding and large-scale private investment to show exactly where the opportunity lies.

Figure 4: The CDR funding and financing landscape mapped against Technology Readiness Levels (TRL 1–9) and Commercial Readiness Levels (CRL 1–9).

Innovation Fund and similar instruments have successfully supported CDR projects through early development. The next step is building the demand-side infrastructure to attract private capital at scale.

Long-term offtake certainty is the missing piece, and it is increasingly within reach.

The answer is taking shape at the EU level, with the EU CRCF Buyers' Club, on which Carbon Gap and Carbon Management Europe published a discussion paper. This mechanism aims at aggregating private demand for high-quality, Carbon Removals and Carbon Farming (CRCF)-aligned credits and turning fragmented buyer interest into the long-term offtake signals projects need to reach FID.

Project developers are making the same case from the inside. Later during the summit, Hafslund Celsio and Stockholm Exergi, pointed to CDR revenues as a concrete way to strengthen CCS project economics signal that the investment case for industrial carbon capture is widening.

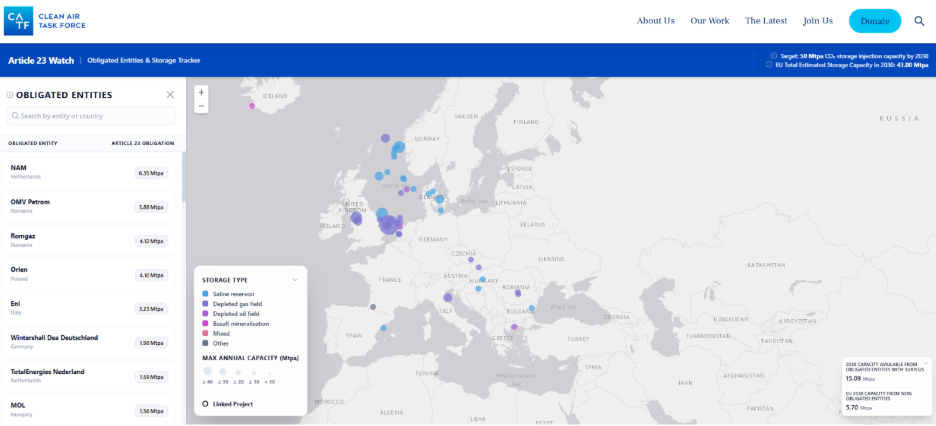

The Article 23 clock is ticking

Under Article 23 of the Net-Zero Industry Act (NZIA), oil and gas producers operating in the EU must contribute to a collective target of 50 Mtpa of CO₂ injection capacity by 2030. Obligated entities have around 6.5 years from the regulation entering into force to comply.

CATF's Article 23 Watch initiative, a joint initiative with Bellona Europa and the Carbon Balance Initiative to track implementation across the EU, was presented by Codie Rossi, Senior Europe Policy Manager for Carbon Management at CATF and Co-Chair of Carbon Management Europe's Policy Working Group.

Figure 5: The Article 23 Watch tracker mapping obligated entities and CO₂ storage projects across Europe. The tool displays each entity's Article 23 obligation in Mtpa alongside available storage capacity by project, type, and location.

Most of the current pipeline of over 40 Mtpa had already begun site characterisation by 2024. Projects such as Prinos and Greensand have already met the NZIA’s 18-month permitting requirement, demonstrating that the timeline is workable in practice and attaining a storage permit within the 6.5-year window is eminently feasible for well-positioned projects.

That said, the majority ofprojects are still waiting for sufficient customer commitments or additional public support before moving forward, and more complex offshore developments will require longer construction periods. The 2030 target is a binding legal obligation, and delays in permitting, financing, and FID create compliance risk for the obligated entities. But the evidence from early movers shows that 2030 remains within reach for projects that move with purpose.

Five things that need to happen

The panel discussion - featuring Kleopatra Avraam (Desfa), Ørjan Jentoft (Aker BP), and Trude Sundset (Norsk Hydro) showed storage is only one part of a broader deployment challenge.

The geographic mismatch between storage capacity and emitters adds real transport complexity and cost across the value chain. Capture, transport, and storage projects all depend on aligned timelines, commercial agreements, and regulatory frameworks, and a delay in one segment quickly affects the others.

Ørjan Jentoft (Aker BP) was also clear that this is not a simple chicken-and-egg deadlock between storage and capture developers. The barriers are more fundamental, and CCS deployment requires sufficient and predictable revenue streams to lift investment across capture, transport, and storage simultaneously.

The session identified five priorities for accelerating deployment:

- Stronger coordination between capture, transport, and storage developers, with aligned timelines and commercial frameworks from the outset

- Faster permitting and more predictable regulatory processes

- Improved bankability across the value chain, with sufficient and predictable revenue streams to support investment in capture, transport, and storage

- Improved market transparency and project-level data sharing, to break the commitment deadlock between storage and capture developers

- Greater cross-border cooperation and infrastructure alignment across Europe, particularly for countries with no domestic storage capacity

Looking ahead

Europe’s CCS pipeline is expanding rapidly. Momentum across both capture and storage is real.

However, momentum alone will not deliver operational projects at scale.

Faster permitting, stronger policy certainty, improved infrastructure coordination, and greater investment confidence will all be necessary to move projects from planning to deployment.

The value chain reality check clearly showed that the bottleneck is not limited to storage alone. Scaling CCS in Europe will require coordinated action across the full value chain, involving industry, policymakers, and financial actors alike.