This paper has been prepared as a discussion document to support the development of EU Carbon Removal Buyers’ Club. It draws on deliberations from closed-door multi-stakeholder workshop convened by Carbon Management Europe and Carbon Gap in February 2026, with the participation of corporate buyers, financial institutions, investors, and policymakers attending in an observer capacity.

The paper maps the principal design options under consideration, discusses the trade-offs associated with each, and reflects the directions that appear most viable in the near term based on the stakeholder dialogue to date. It is not intended as a prescriptive blueprint. The initiative remains under exploration, and all options described herein are subject to further deliberation before any decisions can be taken.

Disclaimer: This document is a working paper for exploratory and discussion purposes only. It does not represent the official position of the European Commission or any participating organisation, nor does it prejudge any future Commission initiative or decision. Views and directions described reflect stakeholder input gathered through consultation and are subject to further deliberation.

Executive summary

The EU Carbon Removal Buyers' Club is a concept under active exploration as a potential mechanism to accelerate the development of a credible, EU-anchored market for carbon dioxide removal (CDR).

The core market challenge is the access to low-cost capital. Capital is available, but not at the cost CDR projects need. In the absence of bankable revenue certainty, the risk perception for CDR projects remains elevated, pushing financing costs to levels that make investment unattractive. As a result, projects cannot reach Final Investment Decision (FID) without credible offtake commitments to bring the risk perception down. A Buyers' Club is explored as a coordination mechanism to aggregate demand, reduce transaction costs, and provide the institutional anchor needed to unlock private investment at scale.

The Carbon Removals and Carbon Farming Regulation (CRCF) has been consistently referenced as the most suitable regulatory foundation, providing the quality and MRV framework upon which buyer confidence can be built. A firm CRCF alignment with flexibility to accommodate future methodologies as delegated acts are adopted appears to offer the most workable balance between credibility and near-term supply availability. A preference emerged for prioritising near-commercial technologies in EU and EEA jurisdictions, with a single club structure accommodating differentiated tracks for permanent and temporary removals.

A corporate-led membership model is considered the most workable near-term configuration, with the club functioning as a coordination hub that leverages existing intermediaries. Ambition is best framed in terms of capital deployed at market formation scale, which is ambitious enough to unlock multiple FIDs and send a credible demand signal, while remaining achievable under current conditions.

The directions described in this paper are working hypotheses, not conclusions, and are subject to further deliberation.

Why a Buyers’ Club for carbon removals?

Carbon dioxide removal (CDR) is widely recognised as an essential component of credible net-zero strategies, both at the corporate level and within European Union (EU) climate policy. Achieving the EU’s 2050 climate neutrality objective is expected to require the large-scale deployment of carbon removals alongside deep emissions abatement across sectors – not as a substitute for emissions reductions, but as a necessary complement to them.

However, the European CDR market remains at an early stage of development. Public funding mechanisms, including the Innovation Fund and national support schemes, have played an important role in supporting early-stage development and deployment. Nevertheless, these instruments do not fully address the commercialisation and scale-up challenges facing the CDR sectors. High capital costs, uncertain revenue streams, evolving regulatory frameworks, and fragmented demand continue to constrain market development. Most critically, commercially bankable private offtake commitments remain limited, restricting the ability of project developers to secure financing and reach Final Investment Decision (FID).

In this context, the concept of an EU Carbon Removal Buyers' Club has been explored as a potential mechanism to coordinate and aggregate demand, de-risk investments, and support the development of more predictable demand signals for high-integrity carbon removals in Europe. By strengthening revenue visibility and improving market coordination, such a mechanism could contribute to lowering perceived project risk and improving access to private capital.

This paper draws on structured multi-stakeholder workshops convened by Carbon Management Europe and Carbon Gap. These workshops brought together corporate buyers, financial institutions, intermediaries, and observers from the European Commission to explore possible design options for such a club, assess associated trade-offs, and identify potentially viable near- and longer-term pathways. The discussions were exploratory in nature, and this paper reflects the state of deliberation as of early 2026.

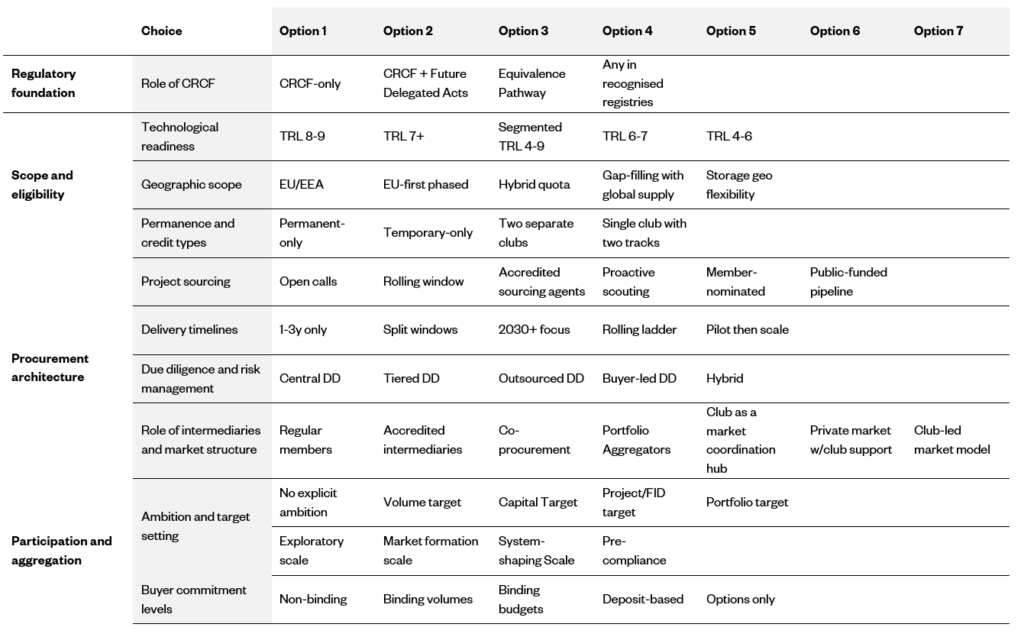

The design space explored across the workshops spans four broad dimensions: the regulatory foundation and role of the Carbon Removals and Carbon Farming Regulation (CRCF), the scope and eligibility of projects and credits, the procurement architecture through which the club would operate, and the participation and demand aggregation model. The table below summarises the principal options considered, which are discussed in subsequent sections.

Table A. Design choice card with options across key dimensions

Regulatory foundation and role of CRCF

A robust regulatory foundation is central to the credibility, eligibility framework, and political viability of a potential EU Carbon Removals Buyers’ Club. Throughout the stakeholder discussions, the CRCF emerged as the most appropriate anchoring framework. The CRCF establishes the quality criteria, monitoring, reporting and verification (MRV) requirements, and institutional processes through which carbon removal activities may be certified within the EU context.

Importantly, the CRCF should be understood as a broader governance and quality assurance framework rather than solely as a certification scheme. It defines the level of rigour expected for eligible carbon removal activities and is expected to play an important role in underpinning buyer confidence, market credibility, and reputational integrity. Yet, the CRCF alone does not create demand for carbon removals. A Buyers’ Club would instead operate as a complementary demand-side coordination mechanism within this emerging regulatory landscape.

As of May 2026, the first set of CRCF methodologies – covering biogenic emissions capture with carbon storage (BioCCS), direct air capture and carbon storage (DACCS), and permanent biochar carbon removal (BCR) – has been adopted by the EU and officially entered into force. Further methodologies remain under development, with the assistance of the Commission Expert Group on Carbon Removals.

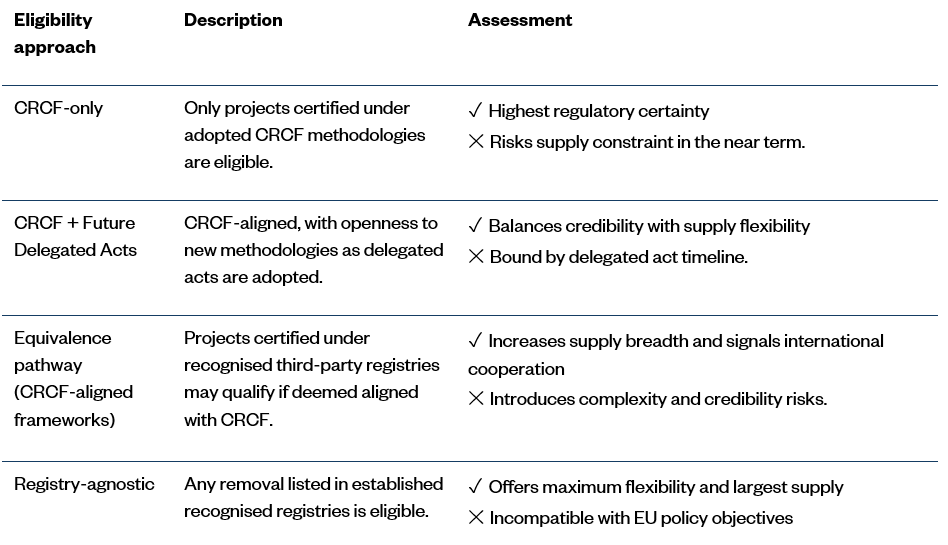

Stakeholder discussions highlighted an important design question concerning the extent to which the Buyers’ Club should be tied exclusively to CRCF-certified activities. An strictly CRCF-based eligibility approach would provide the highest degree of regulatory credibility and reputational robustness. However, given that several methodologies are still under development, such an approach could significantly constrain the near-term supply pipeline available to the club. A more flexible approach – anchoring the club firmly in the CRCF while remaining capable of incorporating additional methodologies as they are adopted through future delegated acts – appears more consistent with the current stage of market development. Several possible approaches are summarised in Table B.

Table B. Regulatory foundation: Overview and trade-offs

A CRCF-only approach offers the highest level of regulatory certainty and reputational robustness but may significantly constrain short-term supply availability. Expanding eligibility to incorporate future delegated acts would preserve alignment with the evolving EU framework while enabling gradual market expansion, although this approach remains dependent on the pace of regulatory development. An equivalence-based model could further increase flexibility and supply diversity but would introduce additional complexity in defining, assessing, and governing comparable standards. By contrast, a registry-based approach could maximise supply in the near term, but would entail substantially greater reputational, governance, and political risks, particularly in the EU context.

The direction that emerged from stakeholder discussions broadly favours a CRCF-aligned but forward-looking approach. Anchoring the club in the CRCF would support credibility, policy coherence, and compatibility with current and future EU regulatory developments, while allowing for the gradual inclusion of additional methodologies as they become available could help avoid unnecessary supply constraints during the market’s early development phase. Such an approach could also position the Buyers’ Club as an early demand-side mechanism supporting the operationalisation and scaling of CRCF-aligned carbon removal markets in Europe.

Scope and eligibility

A clearly defined scope is essential to ensure that the Buyers’ Club can support both market credibility and meaningful scale. Decisions concerning the eligibility of technologies, geographic coverage, and credit types will directly influence the club’s ability to mobilise investment, support EU industrial objectives, and contribute to the development of a high-integrity European carbon removal market.

Technological readiness

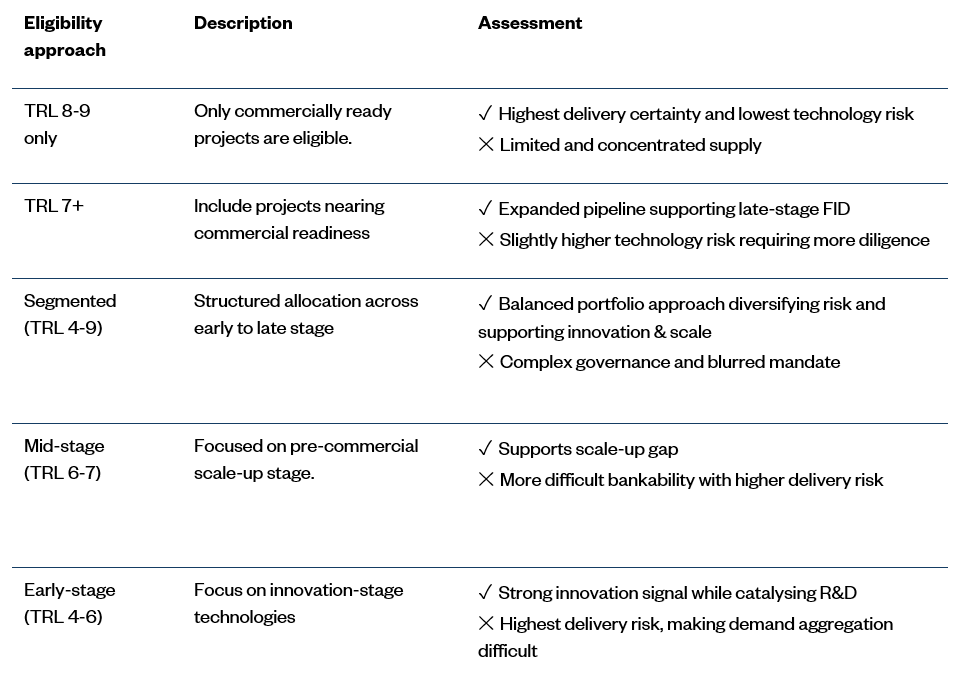

Defining which CDR technologies and approaches should be eligible represents one of the most consequential design choices facing the Buyers’ Club. The range of CDR methods is broad, with significant differences in technological maturity, cost, permanence, scalability, and project risk profiles. Technological maturity– typically assessed through Technology Readiness Levels (TRLs) – is closely linked to project bankability and delivery risk. Several possible approaches are summarised in Table C.

Table C. Eligibility approaches: Technological maturity

A high-TRL approach offers greater delivery certainty for buyers and financiers and is generally more compatible with project finance requirements, but it may limit the available project pipeline. A segmented approach could support a broader range of technologies and innovation pathways, although at the cost of greater governance complexity and risk differentiation. Broader inclusion of lower-TRL technologies may support longer-term innovation objectives but currently appears to sit outside the risk appetite of most buyers and financial institutions.

Stakeholder discussions indicated a strong preference for focusing primarily on technologies that are deployable in Europe today or expected to become commercially operational in the near term, with particular emphasis on higher technology readiness levels (typically TRL 7 and above). The rationale is grounded in both commercial and reputational considerations: buyers and financiers require a reasonable degree of delivery certainty, while the credibility of the club would depend on its ability to support projects capable of delivering verified removals within commercially relevant timeframes.

Nonetheless, stakeholders broadly recognised that earlier-stage technologies are likely to play an important role in the longer-term evolution of the CDR landscape. However, the prevailing view was that these approaches are more appropriately supported through public innovation and R&D funding instruments – including the Innovation Fund and EIC mechanisms – rather than through a Buyers’ Club whose primary purpose would be to facilitate commercially bankable offtake arrangements.

A segmented portfolio approach could be considered, whereby a limited share of procurement is allocated to earlier-stage technologies (TRL 4–9) in order to support innovation and future market development. However, the inclusion of lower-TRL approaches within a commercially oriented Buyers’ Club framework raises important practical considerations. Earlier-stage projects often face higher delivery uncertainty, shorter operational track records, and, in some cases, limited readiness for integration with CO2 transport and storage infrastructure. As technological readiness and delivery horizon are inherently linked, lower-TRL projects would generally require longer-dated forward agreements with differentiated risk-sharing arrangements rather than near-term offtake commitments. In practice, such an approach would be less about expanding near-term supply than about supporting the future development of the project pipeline.

Stakeholders also noted that limited innovation-oriented procurement windows could still play a useful role in specific cases capable of generating valuable operational learning at relatively small scale. If pursued, a segmented approach would likely require clearly defined quotas, dedicated procurement windows, and differentiated governance and risk management arrangements to avoid diluting the club’s core deployment-oriented objective. In parallel, public funding institutions and R&D programmes would continue to play a central role in supporting early-stage technologies and ensuring the development of a robust future project pipeline.

Geographic scope

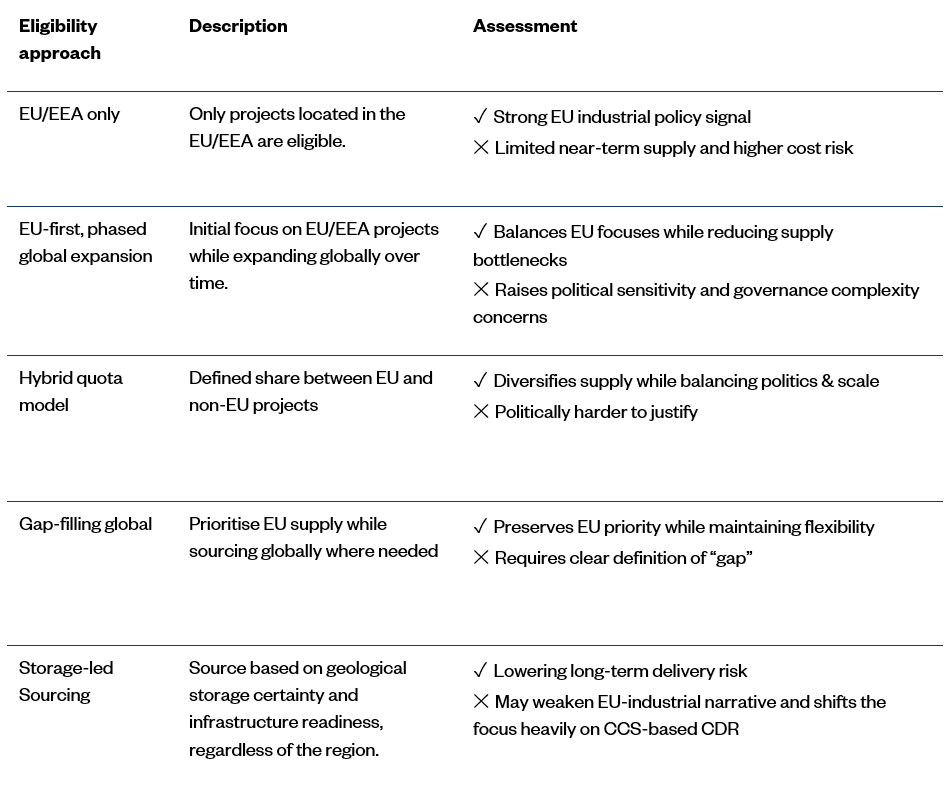

The geographic scope of eligible projects represents one of the more politically sensitive design questions facing the Buyers’ Club, with direct implications for supply availability, industrial policy objectives, strategic autonomy considerations, and regulatory coherence. Several possible approaches are outlined in Table D.

Table D. Eligibility criteria: Geographical scope

An EU-focused approach offers the strongest alignment with EU climate and industrial policy objectives but may constrain supply availability in the near term. A broader international approach could diversify supply and reduce concentration risk, although it would introduce additional complexity relating to monitoring, governance, political acceptability, and alignment with EU industrial strategy. Intermediate “EU-first” approaches may offer a balance between strategic focus and longer-term scalability.

Stakeholder discussions pointed strongly toward prioritising projects located within EU Member States and closely aligned jurisdictions, including the European Economic Area (EEA) and potentially the United Kingdom. This preference was driven by three broad considerations.

- Industrial policy considerations: prioritising European projects could support the development of domestic carbon management industries, infrastructure, and supply chains, while contributing to broader EU objectives relating to industrial decarbonisation coupled with competitiveness objectives, strategic resilience, energy transition, and economic development.

- Policy and regulatory coherence: sourcing within aligned jurisdictions would facilitate consistency with CRCF requirements, the Innovation Fund, and potential future interactions with the EU ETS. By contrast, non-EU sourcing could introduce additional complexity relating to accounting frameworks, nationally determined contributions (NDCs), and Article 6 of the Paris Agreement.

- Demonstration and market-building effects: successful European projects could strengthen confidence among policymakers, investors, and market participants by demonstrating that projects supported through EU policy frameworks are capable of progressing toward commercial deployment and reaching FID.

A broader international scope was not categorically excluded from discussions. Some stakeholders noted that international sourcing may eventually become necessary to achieve sufficient market scale, particularly for removals linked to geological storage resources. However, any expansion beyond Europe would likely require carefully designed equivalence frameworks, governance safeguards, or phased eligibility structures as the market matures.

Permanence and credit types

The treatment of permanence is central to both the environmental integrity and practical usability of carbon removal credits. Different buyers may require different types of removals depending on their emissions profiles, decarbonisation pathways, and climate strategies.

Carbon removal approaches differ significantly in terms of storage characteristics, permanence, monitoring requirements, and reversal risk management. Under the CRCF framework, approaches such as DACCS, BioCCS, and biochar carbon removal (BCR) may qualify as permanent CDR pathways where they meet the applicable methodology and certification requirements.[1] Additional approaches, including mineralisation, enhanced rock weathering (ERW), ocean alkalinity enhancement (OAE), and direct ocean carbon capture with storage (DOCCS), may also qualify as permanent removals as methodologies continue to develop within the CRCF framework.[2] By contrast, many nature-based CDR pathways generally involve shorter storage durations and greater exposure to reversal risks associated with land-use change, ecosystem disturbance, climatic conditions, and long-term management practices.

Permanence should therefore be understood as a spectrum of storage permanence and reversal risk rather than as a purely binary distinction. Nevertheless, distinctions between more durable and less durable removals remain highly relevant in both regulatory and corporate claims contexts. Different possible options for the Buyers’ Club are listed in Table E.

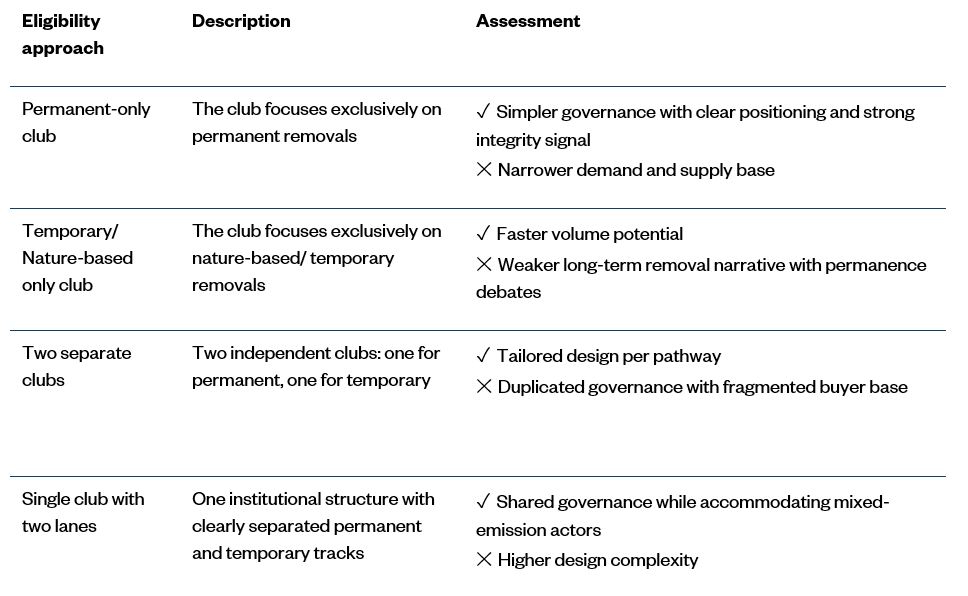

Table E. Eligibility criteria: Permanence

These distinctions matter because buyers may have different strategic objectives and accounting needs. Companies seeking to address residual fossil CO2 emissions within net-zero strategies may prioritise permanent removals. Companies with biogenic, land-use, or shorter-cycle emissions profiles may also have legitimate demand for temporary removals. Yet treating all removals identically risks obscuring important differences in permanence, risk profile, and intended use cases; and creating entirely separate institutional structures for different credit types could increase fragmentation and administrative complexity.

The approach that received the broadest support during stakeholder discussions was a single club structure incorporating differentiated “tracks” for different categories of removals – one for permanent removals and another one for temporary removals. This approach reflects the practical reality that many companies carry both fossil and biogenic emissions and therefore may have legitimate demand for multiple removal types as part of broader climate strategies. A single structure with differentiated tracks would preserve governance, infrastructure, and procurement processes while enabling buyers and suppliers to participate according to the characteristics, intended use cases, and risk profiles of different removal categories.

Procurement architecture

Project sourcing

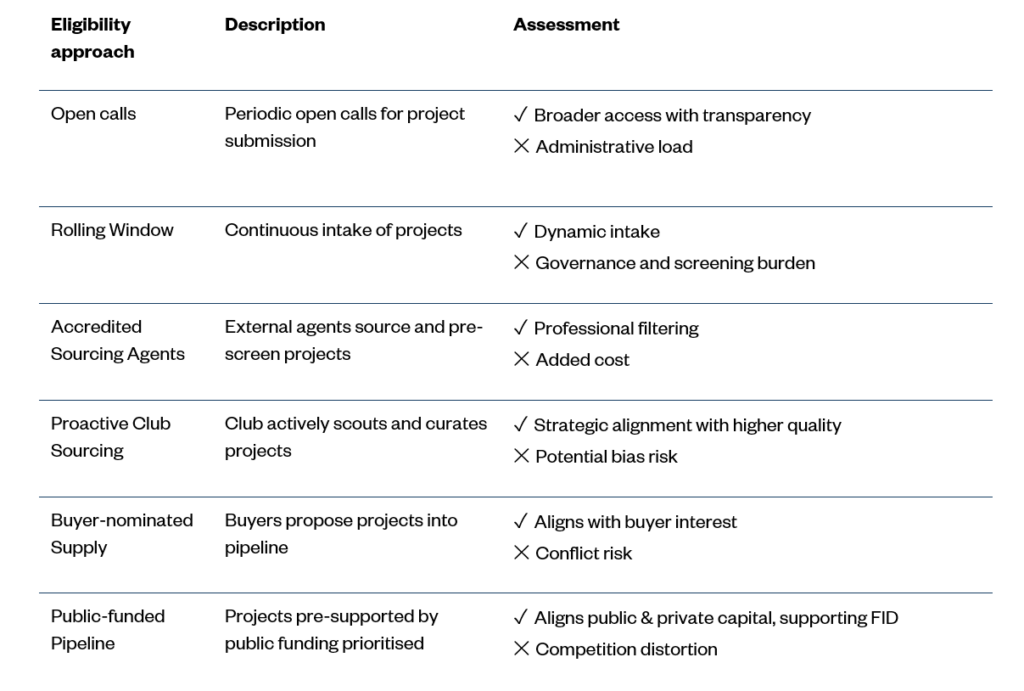

The way in which projects enter the Buyers’ Club pipeline has significant implications for transparency, accessibility, competition, and governance. This question sits at the intersection of market openness and effective quality screening, particularly in a market where the supplier landscape remains relatively nascent and heterogeneous. Several models were examined in stakeholder discussions, ranging from fully open periodic calls to invitation-based processes managed either by the club or through designated intermediaries, as shown in Table F.

Table F. Procurement architecture: Project sourcing

Stakeholder discussions indicated a clear preference for transparent open calls as the primary sourcing mechanism. The underlying rationale was that a European initiative of this nature should operate according to transparent and non-discriminatory access principles, thereby reducing perceptions of favouritism or opaque gatekeeping. Open calls could also support supplier discovery by enabling emerging projects – including those not yet well-connected to established buyer networks – to participate in the procurement pipeline.

Stakeholders acknowledged, however, that open calls alone would not fully address the challenge of quality screening and project assessment. In practice, experienced buyers, intermediaries, and financial institutions would likely continue to undertake various forms of pre-screening and technical evaluation. The club’s governance framework would therefore need to incorporate structured assessment and screening processes capable of complementing open access principles without undermining transparency. A hybrid approach – combining open calls with structured due diligence and technical evaluation processes – emerged as the most operationally credible direction. This issue is explored further in the section on “Due diligence and risk management” below.

Delivery timelines

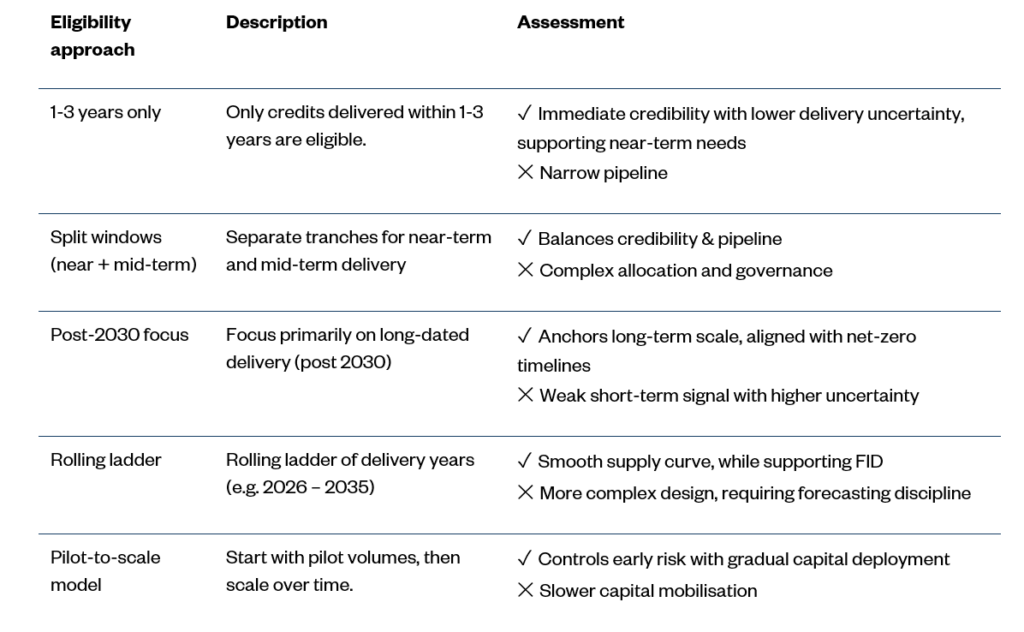

The timing of credit delivery is closely related to, but distinct from, the question of technology maturity. A Buyers’ Club focused exclusively on near-term delivery horizons (for e.g. one to three years) would necessarily be limited to projects that are already at or near- commercial operation. Conversely, a model focused solely on long-dated delivery would likely struggle to generate early market momentum and may be less attractive to buyers operating under nearer-term corporate climate and sustainability objectives. The main approaches considered are summarised in Table G.

Table G. Procurement architecture: Delivery timelines

Stakeholder discussions broadly converged around a model combining both near- and medium-term procurement horizons. Under such an approach, near-term delivery windows could support projects already approaching commercial readiness, while medium-term procurement tranches could align with the development timelines of larger infrastructure-scale projects progressing toward FID.

This “split-window” approach could enable the club both to demonstrate early market activity while simultaneously supporting the pipeline of larger-scale projects expected to represent a substantial share of future European CDR capacity. It also reflects the practical reality that technology readiness and delivery timelines are intrinsically linked: shorter delivery horizons are generally feasible only for more commercially mature technologies, while earlier-stage approaches inherently require longer development and contracting timelines. Ensuring coherence between these dimensions is important to maintaining both the credibility and long-term scale potential of the club.

Due diligence and risk management

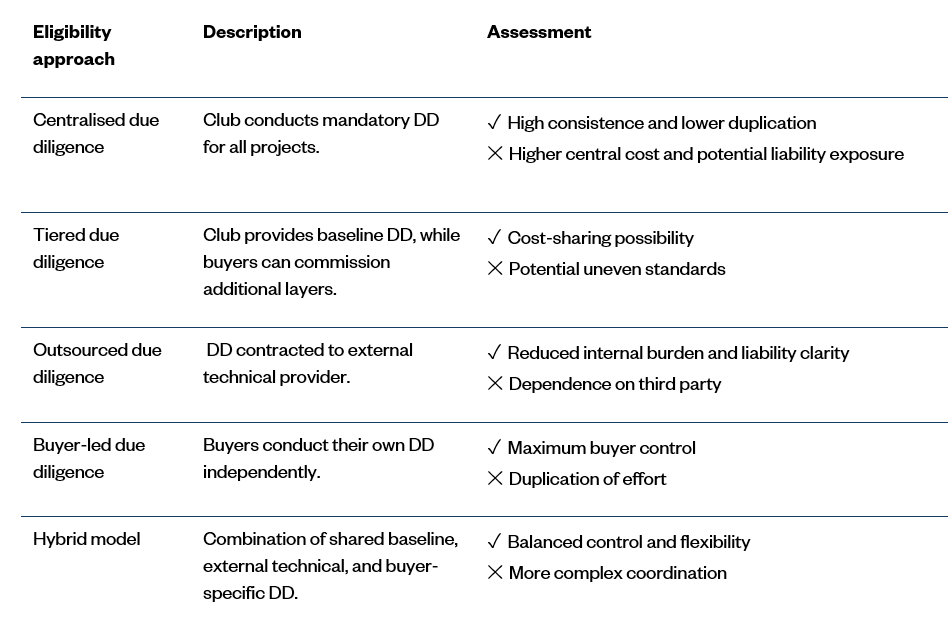

Due diligence (DD) is central to the value proposition of a Buyers’ Club. Buyers require confidence that purchased removals are real, additional, and verifiable. Financiers require project-level analysis before committing debt financing. Smaller or less experienced buyers may also benefit from shared diligence infrastructure capable of reducing transaction costs and improving access to the market. Five broad due diligence models were examined, as shown in Table H.

Table H. Procurement architecture: Due diligence

The direction that emerged from discussions strongly favoured a hybrid model combining shared baseline assessments (designed to minimise potential conflicts of interest) with optional additional layers of technical, financial, or buyer-specific due diligence. This approach reflects the reality that different stakeholders operate under different risk tolerances, governance requirements, and investment criteria. Corporate buyers may place particular emphasis on reputational and claims-related diligence, while financial institutions require detailed project finance and counterparty risk analysis. Intermediaries and technical advisors may also provide specialised expertise relating to technology performance, MRV systems, or storage integrity. No single centralised diligence model is likely to satisfy all these requirements fully. However, a shared baseline framework could substantially reduce duplication, improve market accessibility, and lower transaction costs, particularly for smaller and/or less experienced market participants.

Regardless of the model chosen, participants also stressed that risk management extends beyond initial project assessment and due diligence. Ongoing monitoring between contract signature and credit delivery is essential, particularly for infrastructure-scale projects with long development timelines and construction risk exposure.

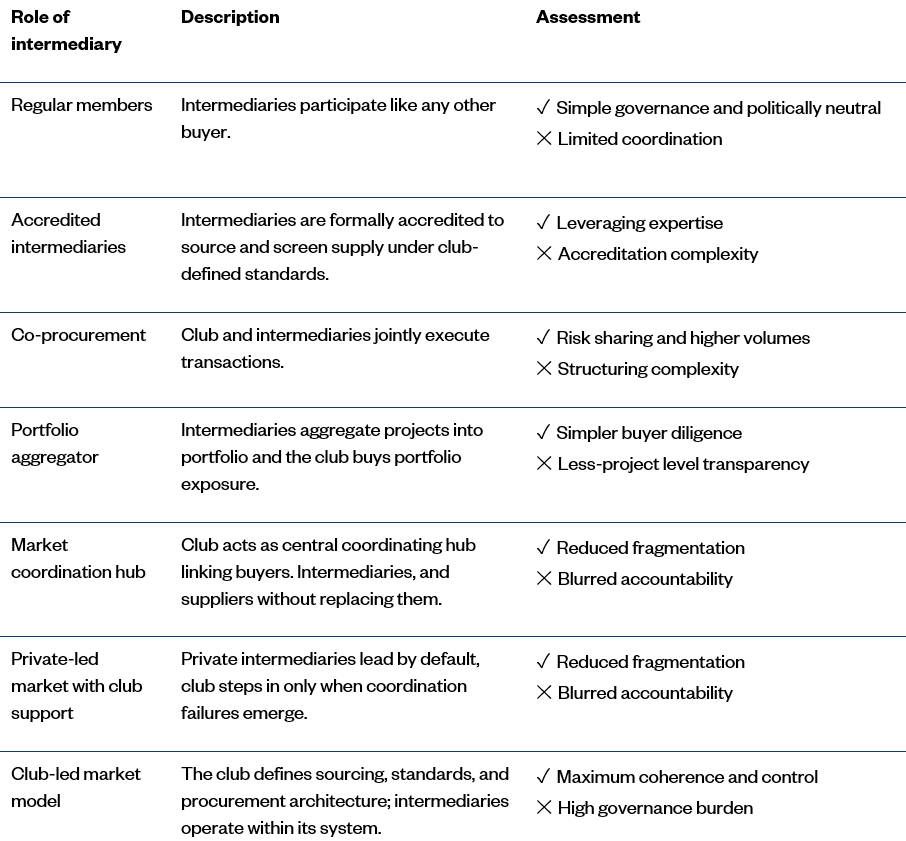

Role of intermediaries and market structure

The current CDR market already features a growing ecosystem of intermediaries, including project aggregators, sourcing platforms and agents, specialised procurement intermediaries and buyers’ clubs, advisory firms, and trading platforms. The Buyers’ Club would therefore not operate in an institutional vacuum, and its design would need to take account of existing market infrastructure and expertise. A central question is how to position the club to complement existing market infrastructure. Several potential approaches were discussed, as outlined in Table I.

Table I. Procurement architecture: Role of intermediaries

Stakeholder discussions generally indicated that the Buyers’ Club should seek to complement rather than replace existing market actors. The current ecosystem already embodies significant technical expertise, due diligence capabilities, supplier relationships, and operational experience. Attempting to replicate these functions centrally could introduce unnecessary complexity and risk undermining existing market development efforts. A more widely supported framing positions the Buyers’ Club as a market coordination and governance platform: providing transparency, common standards, institutional credibility, and demand aggregation, while leveraging existing intermediaries for project sourcing, aggregation, technical assessment, and transaction execution.

Several stakeholders highlighted the potential value of a model in which intermediaries could be formally accredited by the club and operate under clearly defined governance standards, transparency requirements, and participation criteria. Co-procurement arrangements, whereby transactions are jointly structured or facilitated by the club and specialised intermediaries, were also identified as a potentially valuable, especially during the market’s early development phase. Such arrangements could allow the club to benefit from existing market expertise and operational capacity while maintaining a coherent governance framework and ensuring alignment with broader policy and market integrity objectives.

Participation and demand aggregation

The question of participation scope is closely linked to the governance structure, strategic objectives, and operational credibility of the Buyers’ Club. Decisions concerning ambition levels and the nature of buyer commitments will significantly influence the club’s ability to generate credible market signals, support project bankability, and attract broad participation across the emerging European CDR ecosystem.

Ambition and target setting

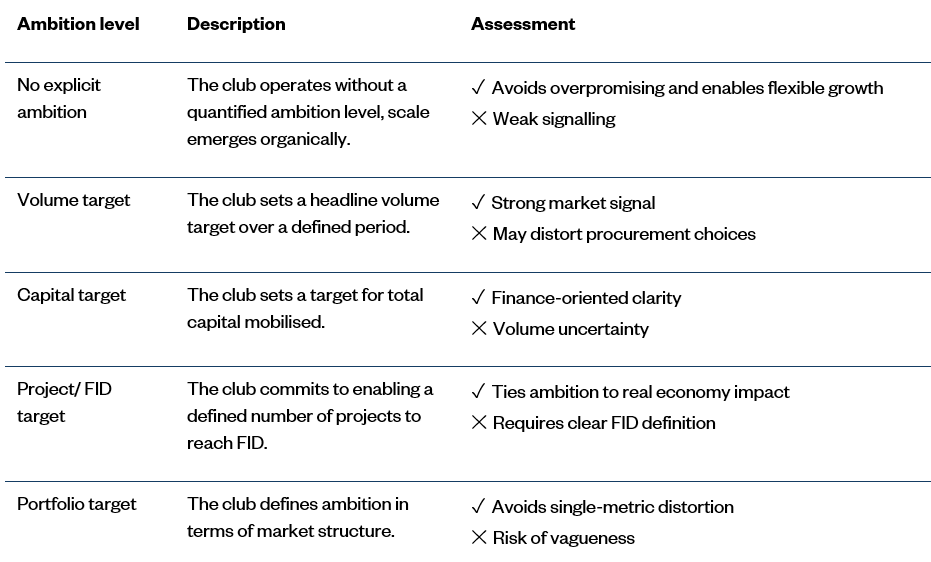

Whether and how to set explicit ambition targets is a strategically important question for the Buyers’ Club. Targets that are perceived as overly ambitious and subsequently missed could undermine market confidence and institutional credibility. Conversely, targets that are too modest may fail to generate sufficiently meaningful market signals or catalyse additional investment and participation. Table J explores different options.

Table J. Ambition levels and target setting

Stakeholder discussions highlighted important trade-offs between different target-setting approaches. Pure volume-based targets may prove challenging in a market characterised by long project development timelines, uncertain delivery schedules, and evolving supply availability. The risk of under-delivery is high, particularly during the market’s early stages.

Project-based or FID-oriented targets may offer greater operational relevance but could be more difficult to aggregate and communicate consistently across technologies and procurement structures. By contrast, capital-based targets – reflecting the aggregate financial commitments of club members associated with procurement activity – appear more closely aligned with project finance realities and the underlying investment needs of the sector. A capital-oriented framing also aligns more naturally with the way both buyers and financial institutions typically assess investment decisions, namely through budget allocations, financing commitments, and long-term procurement planning rather than fixed tonne-based obligations.

The direction that emerged from stakeholder discussions broadly favours framing ambition in terms of capital mobilisation, oriented toward market formation scale: an ambition sufficiently large to unlock multiple FIDs and send a credible market signal, while remaining achievable given current market and policy conditions. Expressing targets through a directional “North Star” framing rather than through rigid numerical thresholds was also viewed as potentially beneficial to help manage the reputational risk associated with public targets, while still signalling long-term intent and providing strategic guidance for the club’s development.

A capital‑based market formation approach offers several potential advantages:

- Flexibility: allows the club to adjust procurement volumes in response to evolving supply availability, price signals, and project readiness without creating excessive pressure to meet fixed volumetric targets.

- Alignment with financing structures: resonates more directly with the budgetary and financing frameworks used by corporate buyers, lenders, and institutional investors, who plan for budgets rather than tonne quotas.

- Scalability: market‑formation scale is large enough to catalyse additional buyers, suppliers, and financing activity while avoiding premature assumptions regarding future compliance market integration (including potential EU ETS integration debates).

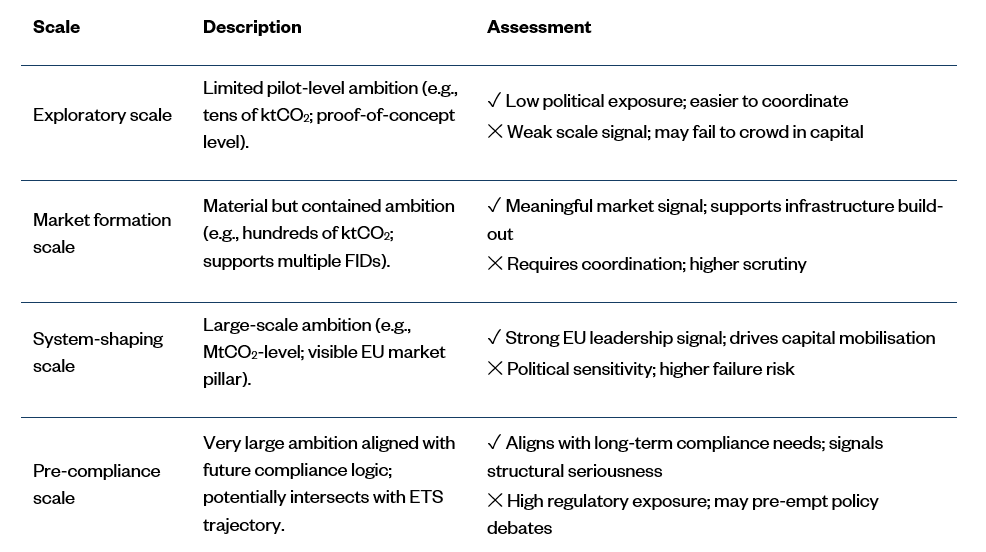

A related but distinct question concerns the overall order of magnitude at which the Buyers’ Club should operate. Table K below sets out the four broad scales considered during stakeholder discussions.

Table K. Order of magnitude of ambition

An exploratory-scale approach was generally viewed as insufficient to generate a meaningful market signal or mobilise additional private capital. At the opposite end of the spectrum, pre-compliance and system-shaping scales – while directionally compelling – were regarded by many stakeholders as potentially premature in the absence of greater regulatory and policy clarity. System-shaping scale raises legitimate questions around political exposure and governance burden that the Buyers’ Club, at this stage of development, may not be equipped to absorb.

A market formation-scale approach (large enough to support multiple FIDs and send a credible demand signal, while remaining operationally and politically manageable under current conditions) emerged as the most workable ambition horizon for the club's initial phase. Stakeholders nevertheless noted that capital commitments should be understood primarily as indicators of market mobilisation and financing confidence rather than direct proxies for delivered removals volumes.

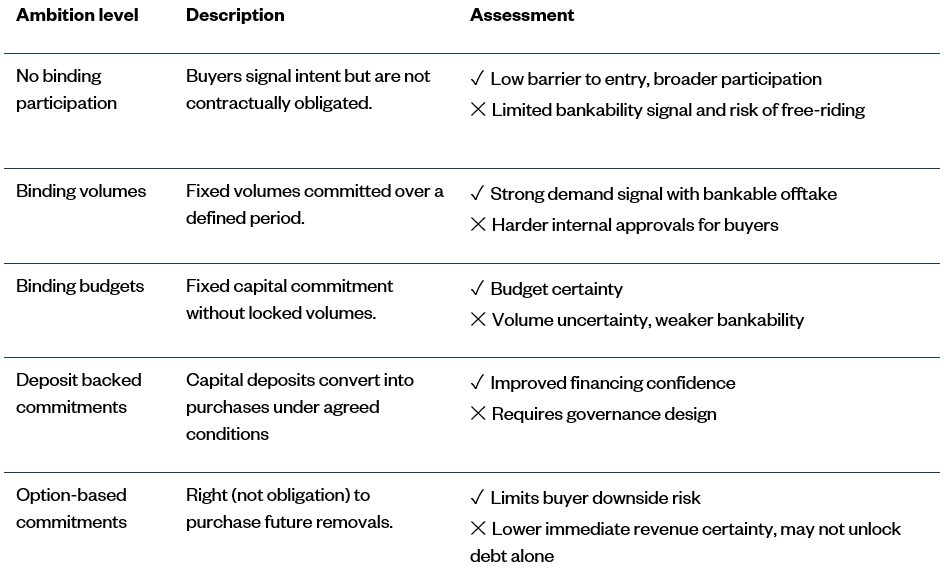

Buyer commitment levels

The strength and structure of buyer commitments will significantly influence the club’s capacity to support project bankability and investment mobilisation. Stronger commitments generate better offtake signals and improve revenue visibility for project developers and financiers, while weaker commitments lower barriers to participation and broaden the pool of potential members but may not provide the revenue certainty that projects need to reach FID.

Stakeholder discussions examined five models for structuring buyer participation and procurement commitments, as described in Table L.

Table L. Buyer commitment levels

Discussion across multiple sessions pointed consistently toward non-binding participation as the appropriate starting point for the club’s initial phase. The rationale was primarily pragmatic: binding procurement obligations are likely to deter participation, particularly among buyers navigating within evolving corporate sustainability strategies and uncertain use cases for CDR credits.

In the near term, the priority should be building a critical mass of engaged buyers. More formal commitment structures could be introduced as the market matures, regulatory clarity improves, and the club develops operational experience and market credibility. This does not mean the club should be indefinitely non-committal. Stakeholders emphasised that a purely networking or learning-oriented structure would not constitute a credible Buyers’ Club. The expectation underpinning the discussions was that an initial non-binding participation model would progressively evolve toward mechanisms capable of generating the more durable and bankable demand signals required to support commercial-scale project finance. This evolutionary approach reflects the broader reality of the European CDR market: institutional structures may need to develop incrementally alongside regulatory frameworks, procurement practices, claims guidance, and market maturity rather than attempting to establish fully mature market arrangements from the outset.

Enablers, constraints, and political landscape

The feasibility and effectiveness of the Buyers’ Club depend, to a significant degree, on developments within the broader European policy and market landscape that remain outside the club’s direct control. Stakeholder discussions identified a number of critical enable conditions, structural constraints, and policy dependencies that are likely to shape both the viability and long-term impact of the initiative.

Claims and use of CDR credits

One of the most frequently cited constraints concerns the absence of clear guidance regarding the claims that corporate buyers may make in connection with the use of CDR credits. In the absence of greater clarity – including on how removals may interact with net-zero strategies, carbon neutrality claims, compensation claims, or broader corporate climate disclosures – many potential buyers face difficulty establishing compelling and sufficiently robust internal business cases for procurement. This issue extends beyond the Buyers’ Club itself and sits primarily within the remit of the European Commission, international standard-setting initiatives, and evolving corporate disclosure frameworks. Nevertheless, stakeholders consistently identified greater clarity regarding claims frameworks and acceptable use cases as an important enabling condition for sustained corporate demand growth.

CRCF methodology development

The pace and scope of further CRCF methodology development will directly shape the supply pipeline available to the Buyers’ Club. The expansion of methodologies covering a wider range of CDR approaches could increase the pool of eligible projects and improve market diversity. Stakeholders also highlighted the importance of transparency regarding the methodology development pipeline itself. Greater visibility concerning methodologies under preparation, indicative timelines, and prioritisation processes could help reduce perceived regulatory uncertainty and improve investment planning and capital allocation decisions.

Potential EU ETS integration

The long-term demand outlook for carbon dioxide removals in Europe may be significantly influenced by future developments relating to the EU ETS, including the possible future integration of certain categories of permanent carbon removals within the compliance framework. Any such integration remains subject to further regulatory and technical assessments as well as political negotiations. Questions relating to environmental integrity, accounting treatment, market impacts, emissions reduction incentives, and broader policy coherence would require careful consideration before any integration pathway could be operationalised. Yet, stakeholders noted that expectations regarding potential future EU ETS integration may already be influencing market behaviour, investment decisions, and long-term strategic positioning within the European CDR sector. The Buyers’ Club would therefore likely need to retain sufficient flexibility to adapt to evolving policy developments and potential changes in market structure over time.

Permitting and infrastructure

For CDR approaches requiring CO2 transport and geological storage infrastructure – including BioCCS and DACCS – the availability of permitted storage sites and access to CO2 transport infrastructure represent fundamental deployment constraints. Progress under the Net-Zero Industry Act, TEN-E framework, CCS Directive implementation, and related European infrastructure initiatives will therefore play an important enabling role for the scale-up of engineered carbon removals. While a Buyers’ Club would not itself be capable of resolving infrastructure bottlenecks directly, stakeholders emphasised that procurement design, project eligibility criteria, and due diligence frameworks should appropriately account for infrastructure access, storage availability, and permitting risk.

Contract standardisation

Transaction costs within the CDR market remain relatively high, partly because procurement processes and contractual arrangements continue to be highly bespoke, resource intensive, and time-consuming. Stakeholders identified significant potential value in the development of more harmonised contractual templates and standardised procurement terms capable of reducing transaction complexity, accelerating negotiations, and lowering barriers to participation, particularly for smaller buyers and newer market participants. The Buyers’ Club could potentially contribute to this standardisation process by facilitating the development and publication of common contractual frameworks, templates, or model agreements that market actors could subsequently adapt to specific project and procurement contexts.

Financing and public-private blending

One of the clearest insights emerging from stakeholder discussions is that the principal financing constraint facing CDR projects in Europe is not the availability of capital itself, but rather the absence of sufficiently predicable and bankable revenue streams capable of supporting commercial project finance structures. Financial institutions participating in the discussions indicated that debt capital may be available for CDR projects where sufficiently robust offtake arrangements and revenue visibility are in place. The Buyers’ Club could therefore contribute directly to improving project bankability by aggregating and formalising demand commitments capable of supporting financing decisions.

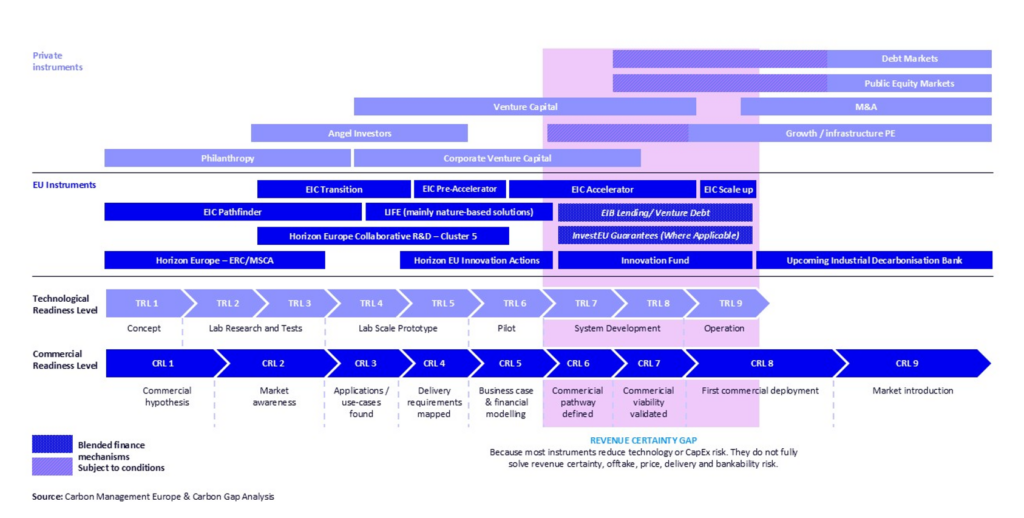

The interaction between public and private financing is particularly important. The European Union already provides substantial supply-side support for carbon removals through instruments such as the Innovation Fund, the EIC Accelerator, European Investment Bank (EIB) lending, and InvestEU guarantees. However, a structural financing gap persists between pilot-scale demonstration and commercial-scale deployment – often referred to as the “missing middle” – where projects may have progressed beyond the scope of traditional R&D support but still lack the revenue certainty required to secure commercial financing (as shown in Figure A).

In this context, the Buyers’ Club could help to close this “revenue stabilisation gap” and serve as a demand-side complement to existing public funding instruments, which would help strengthen market confidence and improve the bankability of projects receiving public support. Rather than duplicating or competing with existing public instruments, the club’s role would be additive: visible private offtake commitments can help validate public spending, strengthen financing cases, and in doing so extend the broader market impact of public investment.

Stakeholders also discussed several potential blended-finance approaches that could merit further exploration. Public anchor procurement by Member States or EU institutions – even at relatively modest volumes – can help catalyse private co-investment by demonstrating institutional confidence in a project or technology. Similarly, price top-up mechanisms could help bridge the gap between market prices and the level needed for project viability in the near term. First-loss guarantees or public insurance instruments could also help reduce perceived risk exposure during the market’s early development phase. These approaches are not mutually exclusive and could potentially be combined through phased or tiered financing structures as the Buyers’ Club develops and the market evolves.

Figure A. Financing journey of nascent technologies

Conclusion

The concept of an EU Carbon Removals Buyers’ Club remains under exploration, and this paper does not seek to resolve the many design questions that remain open. The purpose of this paper is to provide a structured overview of the principal design options currently under consideration, an honest account of the trade-offs involved, and a reflection of the directions that appear most viable based on the stakeholder discussions conducted to date.

Several broad conclusions emerge from these discussions.

- There appears to be a credible market rationale for exploring a Buyers’ Club model in the European context. Across stakeholder discussions, the principal constraint facing the CDR sector was consistently identified not as a lack of capital availability per se, but rather as the absence of sufficiently predictable and bankable revenue streams capable of supporting commercial-scale investment decisions. A well-designed Buyers’ Club could potentially contribute to addressing this challenge by aggregating demand, improving revenue visibility, and supporting the development of more credible offtake structures for emerging projects.

- The Carbon Removals and Carbon Farming Regulation (CRCF) was widely viewed as the most credible regulatory foundation for such an initiative. Anchoring the club within the CRCF framework would support policy coherence, market credibility, and compatibility with the evolving European regulatory landscape, while maintaining sufficient flexibility to accommodate future methodological and market developments. Therefore, all participants agree that the club should be designed to support and reinforce that framework.

- Stakeholder discussions consistently pointed toward the importance of leveraging – rather than duplicating or displacing – existing market infrastructure and expertise. Existing intermediaries, project developers, financial institutions, and procurement platforms already play an important role in the emerging CDR ecosystem, and the Buyers’ Club would likely be most effective if designed as a coordination and market-enabling mechanism operating alongside these actors.

- Stakeholders generally emphasised the importance of maintaining a pragmatic and incremental approach to implementation. The near-term priority should be building momentum. Demonstrating operational credibility through targeted pilot transactions and practical market coordination may prove more valuable than attempting to resolve all institutional and governance questions in advance.

Stakeholder discussions were candid regarding the limitations and risks associated with the initiative. Corporate demand for carbon removals remains constrained by uncertainty surrounding claims frameworks and acceptable use cases. Infrastructure and permitting bottlenecks continue to affect engineered removals pathways. More broadly, any initiative that creates expectations it cannot ultimately fulfil risks undermining confidence in both the Buyers’ Club concept and the wider European CDR market.

These challenges do not necessarily argue against moving forward. Instead, they suggest the importance of a measured and adaptive approach: one grounded in transparency (with a governance structure sufficiently accountable to maintain confidence across all stakeholder groups), operational realism (prioritising demonstrable progress over comprehensive design), and a willingness to develop institutional arrangements progressively as the market and policy landscape evolve.

The discussions reflected in this paper should therefore be understood as part of an ongoing process rather than as definitive conclusions. Further stakeholder engagement, continued policy development, and additional analysis will all be necessary before any specific design choices can be formalised. This paper is can hopefully contribute to that process.